Why Compute Is Not a Commodity

Compute is not a commodity. It is not fungible: one hour of a B200 GPU server can be $3 or $9 depending on the networking, facility, and agreements that come with it.

“Compute is the new oil” sounds provocative, which is why investors and builders keep repeating it. But oil is graded, standardized, and deliverable against a futures contract. Compute has none of that.

Compute is not fungible

Fungibility means one unit is interchangeable with another of the same type. A dollar buys the same thing as any other dollar.

The natural response is that compute just needs grading: filter by GPU model and you have fungibility. But even within a single GPU model, the units are not interchangeable.

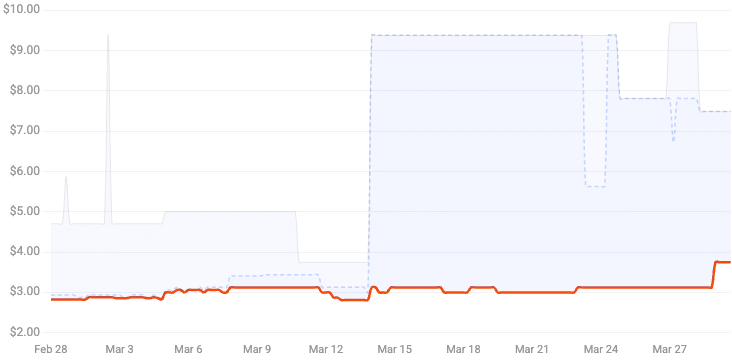

The clearest indicator is the price spread between the cheapest and most expensive listings for a single GPU model. Vast.ai, a large compute marketplace, publishes 30-day price distributions for each GPU-hour they help resell. For B200s in March 2026: the 25th percentile price (25% of listings are cheaper than this price) is $3.18/hr, and the 90th percentile (90% of listings are cheaper) is $9.38/hr.[1]

That's a 3x spread for the same GPU model, on the same marketplace, on the same day.

B200 price trend (30 days)

Across providers, the spread widens further. The H100's rental rates range from $1.49/hr on Vast.ai's marketplace to $6.98/hr on Azure to $10.00/hr on Oracle Cloud.[2] A 6.7x spread for what is nominally the “same” GPU.

H100 pricing across providers, per GPU-hour, early 2026

The spread exists because the GPU is not the product. The product is a whole service that includes: the GPU, server OEM, thermal environment, networking, memory configuration, location, service-level agreements (SLAs), data egress policy, and more.

Two H100s are not interchangeable when one sits on InfiniBand (a high-speed data center interconnect for GPU-to-GPU communication) in a purpose-built cluster and the other is on Ethernet in a budget hosting facility.

What commodity exchanges actually require

Fungibility has been well-defined by commodity exchanges, and we can examine compute from the same perspective.

Gold is the textbook case of perfect fungibility. One troy ounce of gold at 99.5% purity is identical to another troy ounce at 99.5% purity. CME gold futures specify 100 troy ounces, minimum 99.5% fineness, delivered to an exchange-approved vault. The buyer does not care which mine produced it, which refiner processed it, or which vault stored it.

Most traded commodities are not perfectly fungible. They are imperfectly fungible, made tradeable through grading systems. 3,000 cows of a specified breed, weight range, and USDA quality grade are similar enough to another 3,000 meeting the same specs. CME Live Cattle futures specify delivery of 40,000 pounds of USDA-graded steers within defined yield grade and weight ranges.[3] The grading creates fungibility.

CME wheat futures use US No. 2 Soft Red Winter as the basis grade for pricing.[4] The USDA defines tolerances for test weight, moisture content, and kernel damage. Other grades (No. 1, No. 3) are deliverable at premiums or discounts.

Every traded commodity shares five requirements:

- A governing body defines grades with measurable tolerances

- An exchange specifies which grade is the basis

- Premiums and discounts handle deviations from the basis

- Delivery happens at standardized locations with standardized procedures

- And most importantly, the gap between the best and worst deliverable grade is small enough that the premium/discount system works

Obviously, compute has none of this infrastructure and the industry does not seem to be heading in that direction. Every user and use case has a different configuration, and OEMs benefit from a lack of standard.

| Commodity | Fungibility | Grading body | Basis | Price spread |

|---|---|---|---|---|

| Gold | Perfect | LBMA / COMEX | Exists | <1% |

| WTI Crude Oil | Near-perfect | CME / API | Exists | ~5% |

| Wheat | Imperfect | USDA | Exists | ~10-15% |

| Live Cattle | Imperfect | USDA | Exists | ~15-20% |

| GPU Compute | None | None | No standard | 2-8x (200-700%) |

Where compute is narrowly fungible

Single-node, single-model spot rentals approach fungibility. If you need one H100 for four hours to work-on a small model, any H100 with 80GB of VRAM works. Vast.ai, Lambda, and RunPod serve this market. You pick a GPU model, rent by the hour, and do not care which specific provider you get.

This is real fungibility, but the scope is narrow. It covers small researchers and hobbyists.

The moment you need more than one node in larger enterprise workloads, fungibility breaks. The networking between GPUs matters as much as the GPUs themselves for distributed training and large-scale inference; and networking massively varies depending on your use case and provider.

Enterprises don't buy GPU-hours

Enterprises buy clusters: specific GPU counts, specific interconnects, specific locations, specific SLAs, specific contract terms.

A 512-GPU B200 cluster with NVLink in Northern Virginia is not substitutable for 512 discrete H100s scattered across three data centers. A training job that needs GPUs communicating as a single fabric will not run on disconnected nodes, regardless of total GPU count.

Same GPU count, completely different product

| Enterprise cluster | Spot marketplace GPUs | |

|---|---|---|

| GPU count | 512x B200 | 512x B200 |

| GPU-GPU bandwidth | 900 GB/s (NVLink) | None |

| Inter-rack network | 400 Gb/s InfiniBand | Ethernet |

| Topology | High-performance fabric | Basic networking |

| Location | One facility | Multiple sites |

| SLA | 99.99% uptime | None guaranteed |

| Distributed training | Yes | No |

| Effective price | ~$6-10/GPU-hr | ~$3.00/GPU-hr |

Enterprise contracts are bespoke. CoreWeave posted a $66.8 billion backlog of contracted future revenue in its 2025 earnings report.[5] Each contract specifies GPU type, cluster size, location, networking configuration, SLA terms, and pricing. None of these contracts are interchangeable with each other.

Because compute is not fungible, it's not well suited for futures and derivatives. You cannot offset one enterprise compute contract against another on an exchange the way you offset wheat futures.

How a compute future would actually trade

Here's a thought experiment. Let's say you have a compute buyer, maybe an enterprise, that needs compute in 2026, and is worried prices will go up by then. On the other side, you have a seller, maybe a neocloud, that has compute, but is worried prices will go down by then.

Then a futures exchange lists a standardized futures contract: “1,000 H100 GPU-hours, deliverable in Q3 2026.” The buyer locks in the price for that thousand hours far in advance. The counterparty, the seller, receives that payment but must deliver the qualifying compute on that timeline.

The seller has an incentive to deliver the cheapest qualifying GPU-hours: single H100 PCIe cards, no NVLink, budget hosting, high-latency location. The contract technically “delivered” the 1,000 H100 GPU-hours as promised, but the enterprise cannot run the training workload they had in mind.[2]

In wheat futures, the gap between No. 1 and No. 3 grade is narrow enough that the premium/discount system absorbs it. In compute, the gap between an H100 PCIe card at $1.49/hr and an H100 SXM in a DGX cluster at $6.16/hr is the difference between an enterprise training run being on time or late.

Why compute price indices are unreliable

The fungibility issue also impacts compute indices. Spot prices on Vast.ai mix hobbyist nodes (consumer GPUs, residential internet, no SLA) with enterprise-grade hardware (data center GPUs, NVLink, professional support). An average of these prices is meaningless for any specific buyer.

H100 pricing: $1.49/hr at the Vast.ai marketplace floor, $6.98/hr on Azure.[2] An index averaging these tells you the “price of an H100-hour” the way averaging a studio apartment in Long Island with a penthouse in Manhattan tells you the “price of a home.”

Here's another thought experiment. Let's say you're a mid-sized startup that signs a contract with flexible pricing (rates change daily) based on a compute index. The index blends prices on Vast.ai, mostly at $1.49/hr from unreliable operators; which is good for you at signing. But then Vast.ai collects more data and gets ahold of data on several enterprise transactions at $6/hr for high-end networked clusters. It ends up blending to $3/hr, double what you expected at signing. Should you be subject to rates for an entirely different, higher-end product?

Better financial products for compute

Physical infrastructure has been financed for centuries without fungibility or futures markets. Highways, bridges, toll roads, ports, pipelines, power plants. None of these assets are fungible. Each is unique, with specific characteristics and location-dependent economics. Nobody trades highway futures.

The proven structure is a revenue bond: a bond backed by the cash flow a specific asset generates. A toll road authority issues bonds backed by toll collections from a specific highway.[6] Investors evaluate the traffic projections, the toll rates, the maintenance costs, and the geography. They do not need the highway to be interchangeable with other highways. They need the tolls to cover the debt service (the periodic principal and interest payments on the bond).

GPU-backed lending works the same way. CoreWeave secured a $7.5 billion debt facility led by Blackstone and Magnetar in May 2024, collateralized by specificGPU hardware and assigned customer contracts.[7] Apollo backed $5.4 billion for Valor and xAI in January 2026.[8] Nscale signed a $1.4 billion DDTL in February 2026.[9] Each deal is secured by specific hardware, in a specific facility, generating specific contracted revenue.

ABS (asset-backed securities) structures extend this further. Pool GPU-backed loans, tranche the risk into layers (senior debt for conservative investors, equity tranches for those seeking higher returns), and sell to institutional investors. This is the same structure that finances auto loans, mortgages, and equipment leases.

The financial infrastructure for non-fungible physical assets already exists. It financed the Interstate Highway System, the transcontinental railroad, and every toll bridge in America. GPU clusters are the same kind of asset, not a commodity.

Bonds backed by contracted GPU revenue from specific customers

Precedent: Toll road bonds, airport revenue bonds

Loans secured by hardware + assigned customer contracts

Precedent: CoreWeave $7.5B (Blackstone), Nscale $1.4B DDTL

Pool GPU loans, tranche by risk, sell to institutional investors

Precedent: Auto loan ABS, equipment lease ABS

Standardized contracts traded on an exchange, focused on deliverable commodities

Precedent: Gold, oil, wheat futures

References

- ComputePrices.com, Vast.ai GPU pricing data (March 2026)

- IntuitionLabs, "H100 Rental Prices Compared: $1.49-$6.98/hr Across 15+ Cloud Providers" (2026)

- USDA, Commodity Standards and Grades

- CME Group, Chicago SRW Wheat Futures Contract Specifications

- CoreWeave Q4/FY2025 earnings report and SEC S-1 filing

- FHWA, "Highway Bonds: An Emerging Option for Increasing Highway Financing" (1995)

- Blackstone, "CoreWeave Secures $7.5 Billion Debt Financing Facility Led by Blackstone and Magnetar" (May 2024)

- Apollo, "Apollo Backs $5.4 Billion Valor and xAI Data Center Compute Infrastructure Transaction" (January 2026)

- Nscale, "$1.4bn Delayed Draw Term Loan Backed by GPUs" (February 2026)

Frequently Asked Questions

Is GPU compute a commodity?

No. GPU compute lacks the fungibility, standardized grading, and delivery specifications that commodity exchanges require. A B200 GPU-hour is not interchangeable with an H100 GPU-hour, and even identical GPU models trade at 2-8x price spreads depending on networking, location, and provider.

Why can't compute be traded on a futures exchange?

Futures contracts require standardized, fungible units. Commodity exchanges like the CME define basis grades (e.g., US No. 2 Soft Red Winter wheat) with tight tolerances. GPU compute has no governing body for grades, no basis grade, and price spreads of 200-700% between GPU models, making standardized futures contracts impractical.

How should compute infrastructure be financed?

GPU infrastructure is better financed through structures that do not require fungibility: revenue bonds backed by contracted cash flows, GPU-backed lending secured by specific hardware and customer contracts, and asset-backed securities. CoreWeave secured $7.5 billion from Blackstone in May 2024 using this approach.

What makes a commodity fungible?

Fungibility means one unit is interchangeable with another of the same type. Gold at 99.5% purity is perfectly fungible. Imperfect commodities like wheat and cattle are made tradeable through grading systems maintained by bodies like the USDA, with defined tolerances and premium/discount schedules for deviations.

We structure residual value insurance solutions for NVIDIA GPUs, so that equipment finance companies can safely book GPU residuals, and so that neoclouds can get better financing.

Get in touch →